Inaccurate forecasting of demand or production requirements can lead to inefficiencies, such as overproduction, underproduction, or excess inventory. This can result in increased costs due to wasted resources or lost sales opportunities. Here are some common causes of efficiency variance in manufacturing processes. A positive material yield variance means that the company has used less material than expected, indicating that its processes are efficient and its employees are minimizing waste.

2: Compute and Evaluate Materials Variances

If the current equipment cannot meet demand or lacks the necessary capabilities to produce high-quality products, it may be time to invest in new equipment. New equipment may be more efficient and better able to handle high volumes or complex processes, improving efficiency and reducing variance. This involves working with suppliers to ensure that materials are delivered on time and in the right quantities. It also involves optimizing transportation and logistics to reduce delays and improve efficiency. Data should be collected and analyzed to identify areas for improvement and make informed decisions.

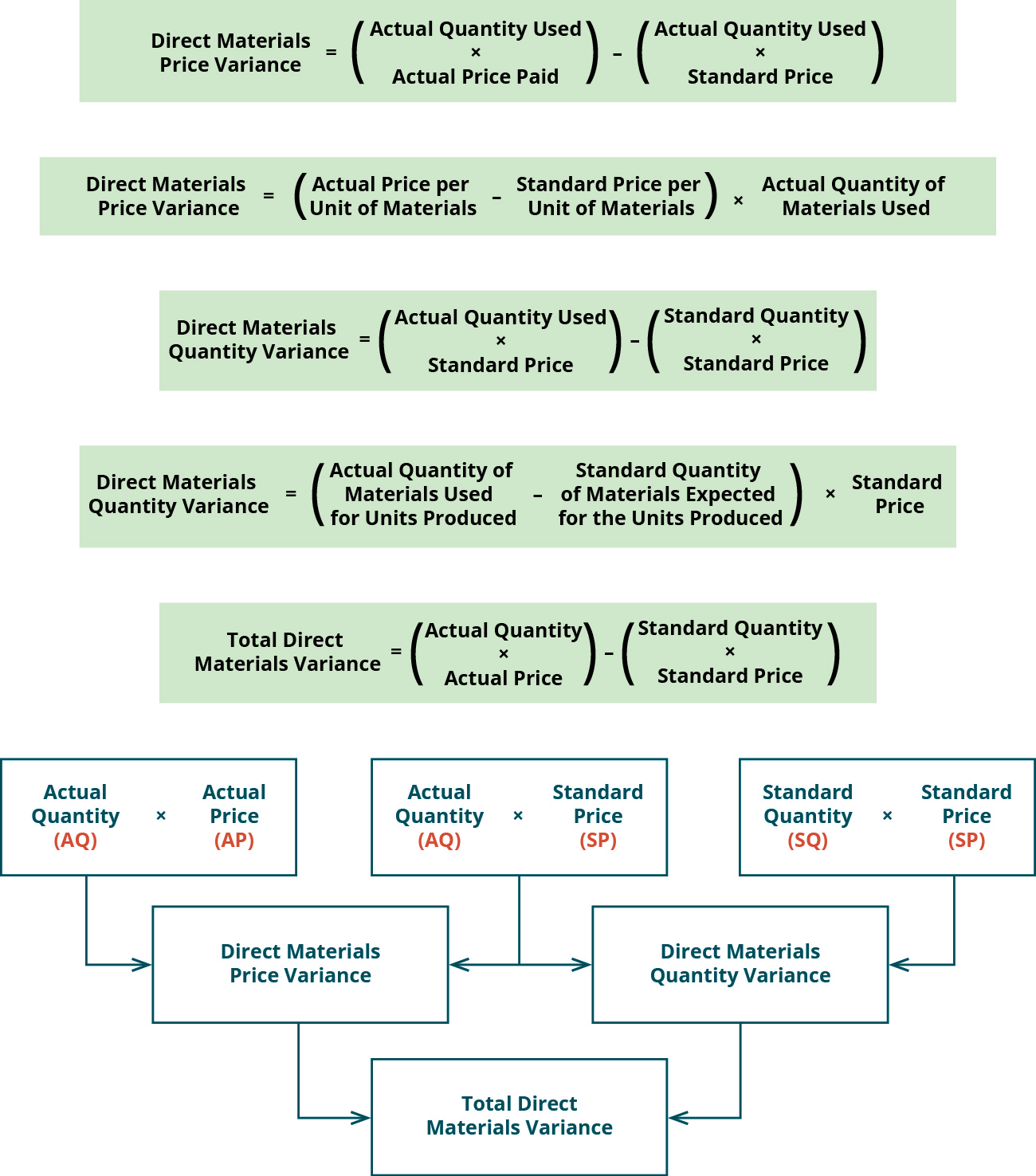

Total Direct Materials Cost Variance

- Although the product was selling well, product costs were higher than expected, translating into lower profits.

- This can occur when employees are not properly trained on the operation of equipment, safety procedures, or quality control standards.

- There are two components to a direct materials variance, the direct materials price variance and the direct materials quantity variance, which both compare the actual price or amount used to the standard amount.

- This involves regularly reviewing processes and procedures to identify areas for improvement and implementing changes to address any issues.

- The program should include both classroom and hands-on training to ensure that employees understand the concepts and can apply them in the workplace.

Variances are favorable if the standard amount is more than the actual amount. When using the template format presented in this chapter, positive variances are favorable and negative variances are unfavorable. In the NoTuggins example, the total standard direct materials allowed was 630,000 feet.

Discover more from Accounting Professor.org

Figure 8.3 shows the connection between the direct materials price variance and direct materials quantity variance to total direct materials cost variance. In this case, the actual quantity of materials used is 0.20 pounds, the standard price per unit of materials is $7.00, and the standard quantity used is 0.25 pounds. This is a favorable outcome because the actual quantity of materials used was less than the standard quantity expected at the actual production output level. As a result of this favorable outcome information, the company may consider continuing operations as they exist, or could change future budget projections to reflect higher profit margins, among other things. At the end of the current operating cycle, Brad determined that the actual variable manufacturing costs incurred to produce 150,000 units of NoTuggins were $181,500 more than the standard costs projected.

Big Data Analytics – Role of Technology in Reducing Efficiency Variance

A debit balance is an unfavorable balance resulting from more direct materials being used than the standard amount allowed for the good output. An unfavorable outcome means the actual costs related to materials were more than the expected (standard) costs. If the outcome is a favorable outcome, this means the actual costs related to materials are less than the expected (standard) costs. With this figure in hand, management can make adjustments to overheard and other factors. But on the other hand, if only 45 labor hours were actually used, then the efficiency variance would be +5, indicating that the manufacturing process was more productive and cost-effective than initially assumed. The organization spent $135,000 for the direct labor hours that exceeded the standard number of hours allowed.

Since this measures the performance of workers, it may be caused by worker deficiencies or by poor production methods. Labor mix variance is the difference between the actual mix of labor and standard mix, caused by hiring or training costs. An example is when a highly paid worker performs a low-level task, which influences labor efficiency variance. The variable manufacturing overhead variances for NoTuggins are presented in Exhibit 8-10 below.

A manufacturer must disclose in its financial statements the amount of finished goods, work-in-process, and raw materials. During the planning stages, the management staff might have projected that it will take 50 labor hours to produce one unit of a specific product. However, after the first round of products is completed, records indicate that 65 labor hours were used, to complete the item in question.

Like direct materials price variance, this variance may be favorable or unfavorable. On the other hand, if workers use the quantity that is more than the quantity allowed by standards, the variance is known as unfavorable direct materials quantity variance. The standard cost of actual quantity purchased is calculated by multiplying the standard price with the actual quantity.

This team of experts helps Finance Strategists maintain the highest level of accuracy and professionalism possible. At Finance Strategists, we partner with financial experts to ensure the accuracy of our financial content. Finance Strategists has an advertising types of irs penalties relationship with some of the companies included on this website. We may earn a commission when you click on a link or make a purchase through the links on our site. All of our content is based on objective analysis, and the opinions are our own.

Examples of indirect materials are items such as nails, screws, sandpaper, and glue. Indirect materials are included in the manufacturing overhead category, not the direct materials category. The production manager oversees the manufacturing process and meets production targets. The production manager works closely with other departments, such as finance, engineering, and quality control, to ensure that production processes are efficient and cost-effective.

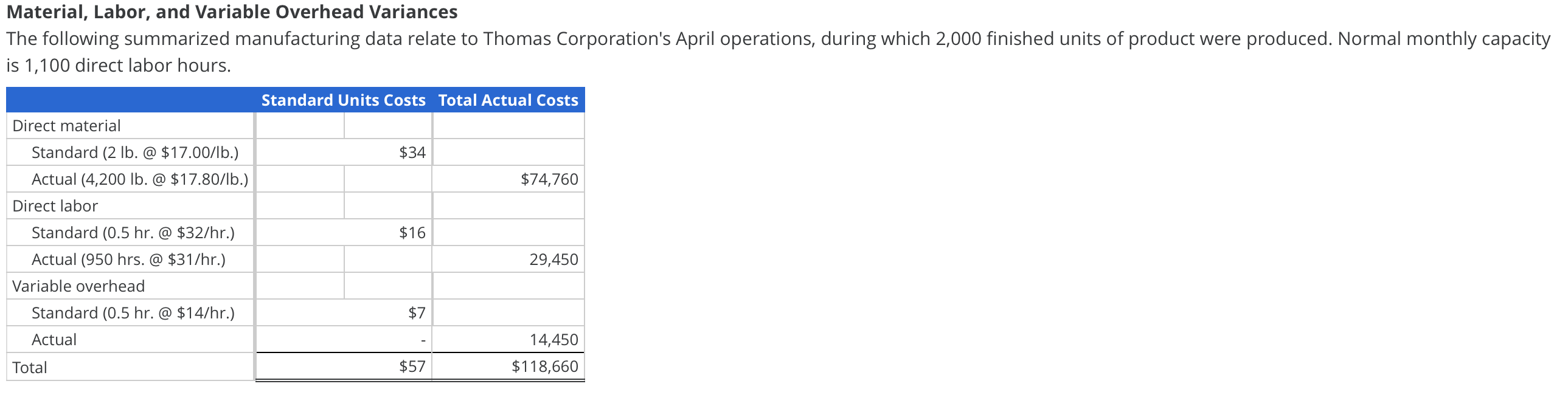

Although the product was selling well, product costs were higher than expected, translating into lower profits. Brad decided to conduct a standard costs variance analysis to see if he could isolate the issue, or issues. The standard costs to make one unit of NoTuggins and the actual production costs data for the period are presented in Exhibit 8-1 below. Recall that the standard cost of a product includes not only materials and labor but also variable and fixed overhead. It is likely that the amounts determined for standard overhead costs will differ from what actually occurs.